Nepal's budget for fiscal year 2083-84, announced in Jestha 2083, introduces a structural overhaul of the personal income tax slab. The new framework doubles the lowest tax band, removes the 30% rate, and collapses the old upper surcharge structure - which previously applied 36% up to Rs 50 lakh and 39% above that - into a single 29% top rate. For salaried employees across Nepal - whether in Kathmandu corporate offices, Pokhara trading firms, or manufacturing plants in Birgunj - the change translates into material take-home pay increases from Shrawan 1, 2083.

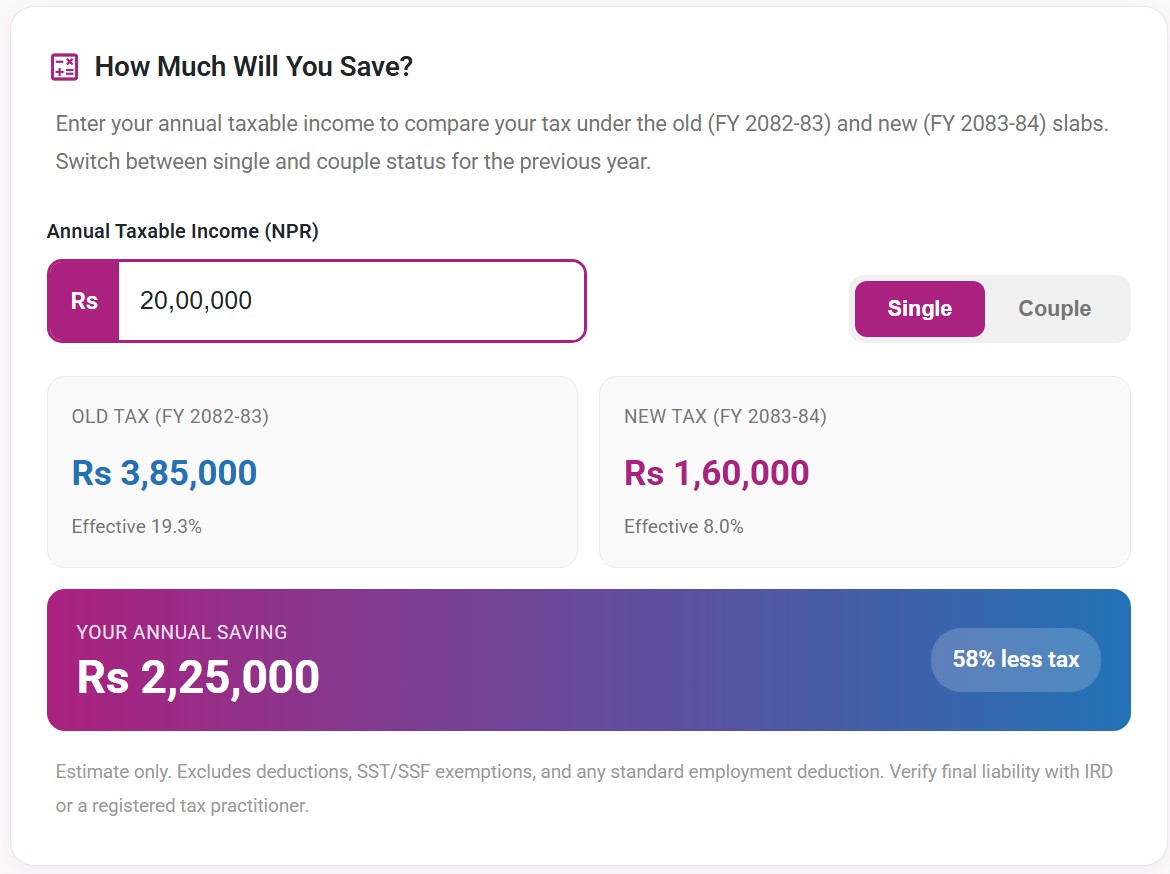

Enter your annual taxable income to compare your tax under the old (FY 2082-83) and new (FY 2083-84) slabs. Switch between single and couple status for the previous year.

The revisions directly affect every employer's TDS obligation under Section 87 of the Income Tax Act 2058. Businesses running payroll must recalculate monthly withholding before the new fiscal year opens. Employees who want to plan annual tax liability accurately will need the new numbers from the first payslip. This article provides a direct side-by-side comparison of the old and new slabs, worked examples at common salary levels, and a clear action checklist for employers and employees alike.

All figures reflect the rates announced in the FY 2083-84 budget. Confirm final rates with the Inland Revenue Department (IRD) or a registered tax practitioner before filing - Finance Acts can carry late amendments that alter specific provisions after the initial budget announcement.

Old Slabs vs New Slabs - A Direct Comparison

Nepal's personal income tax structure for FY 2082-83 applied six bands to individual salaried income. The first band (1%) was technically a Social Security Tax (SST) on income up to Rs 5 lakh - employees already contributing to SSF were exempt from this band. Above that, four regular income tax bands applied: 10% on the next Rs 2 lakh, 20% on the next Rs 3 lakh, 30% on the next Rs 10 lakh, and then two surcharge rates: 36% (base 30% plus 20% surcharge) on income from Rs 20 lakh to Rs 50 lakh, and 39% (base 30% plus 30% surcharge) on all income above Rs 50 lakh. A person earning Rs 12 lakh paid 30% on Rs 2 lakh of their income. Anyone above Rs 50 lakh faced a 39% effective rate on the excess.

The FY 2083-84 structure replaces all six bands with five wider, lower brackets and no surcharge mechanism. The table below places the two systems side by side:

| FY 2082-83 Slab (NPR) | Old Rate | FY 2083-84 Slab (NPR) | New Rate |

|---|---|---|---|

| First Rs 5,00,000 | 1% (SST) | First Rs 10,00,000 | 1% |

| Rs 5,00,001 - Rs 7,00,000 | 10% | Rs 10,00,001 - Rs 15,00,000 | 10% |

| Rs 7,00,001 - Rs 10,00,000 | 20% | Rs 15,00,001 - Rs 25,00,000 | 20% |

| Rs 10,00,001 - Rs 20,00,000 | 30% | Rs 25,00,001 - Rs 40,00,000 | 27% |

| Rs 20,00,001 - Rs 50,00,000 | 36%* | Above Rs 40,00,000 | 29% |

| Above Rs 50,00,000 | 39%** |

* Effective 36% = 30% base + 20% surcharge on income between Rs 20L and Rs 50L. ** Effective 39% = 30% base + 30% surcharge on income above Rs 50L. The 1% first band is a Social Security Tax (SST); SSF contributors were exempt from SST.

For married couples, the FY 2082-83 structure started the 1% band at Rs 6 lakh (vs Rs 5 lakh for individuals), with subsequent bands adjusting accordingly. 2083-84 Finance Act removed the concept of couples in the new structure The rates in the table above apply to both individual and couple taxpayers as announced in the budget.

The 2083-84 revision is not a marginal adjustment. Every bracket threshold has shifted substantially upward, the 30% band disappears, and the old surcharge rates of 36% and 39% are replaced by a flat 29% above Rs 40 lakh. The combined effect reaches every salaried person earning above Rs 5 lakh per year.

How Much Do You Save - Calculations at Common Salary Levels

Rates matter, but the practical impact is clearest at real salary levels. The examples below apply each slab system in sequence to gross annual salary and show the tax liability under both structures. No deductions are included - these are baseline numbers before any claim for life insurance premiums, SSF voluntary contributions, or other allowable deductions under the Income Tax Act 2058. Your actual tax will be lower if you hold qualifying deductions.

Nepal's fiscal year runs from Shrawan 1 to Ashadh end. The new tax slabs take effect from Shrawan 1, 2083 (mid-July 2026). Income earned in FY 2082-83 - even if paid in Shrawan after the date change - is taxed under the old structure. The annual return filed in Ashwin 2083 for the 2082-83 year uses the old rates. The first payslip that applies the new slabs is the Shrawan 2083 payslip. Both employer and employee need to act before that date.

At Rs 10 lakh annual salary, the old structure produced a tax of Rs 85,000 (Rs 5,000 at 1%, Rs 20,000 at 10%, Rs 60,000 at 20%). Under the new slab, the entire Rs 10 lakh falls within the 1% band - tax drops to Rs 10,000. Annual saving: Rs 75,000. At Rs 15 lakh, the saving is approximately Rs 1.75 lakh - tax falls from Rs 2.35 lakh to just Rs 60,000. At Rs 25 lakh, the reduction is roughly Rs 3.05 lakh (from Rs 5.65 lakh to Rs 2.60 lakh), a saving of over 54% on the same income. At Rs 40 lakh, the annual saving is approximately Rs 4.4 lakh. The biggest percentage benefit falls on earners in the Rs 8-15 lakh range, who shift from paying 20% on their upper income to the 1% band entirely.

Earners in the Rs 8-15 lakh range see the sharpest percentage improvement - previously caught in the 20-30% bands, they now sit entirely within the 1% or 10% zone. Employers running payroll for mid-level staff should recalculate TDS before Shrawan 2083 - the difference in monthly withholding is substantial.

TDS Impact for Employers - What Payroll Teams Must Do Before Shrawan

Under Section 87 of the Income Tax Act 2058, employers must deduct tax at source from employee salaries each month based on the estimated annual tax liability. This monthly TDS is calculated by projecting the full year's salary, computing annual tax using the current slabs, and dividing by 12. The new slabs mean that for most employees, the correct monthly TDS from Shrawan 2083 will be substantially lower than in previous months. Running Shrawan payroll with the old slab table is not a minor error - at a salary of Rs 10 lakh, the old slab produces Rs 85,000 annual tax versus Rs 10,000 under the new structure. That is a Rs 75,000 over-deduction across the year, which the employee will need to claim back at return time.

Applying old slab rates to FY 2083-84 payroll is a TDS computation error. Over-deduction creates unnecessary refund work for employees. Under-deduction - if any part of the slab was set incorrectly - creates personal tax liability at year-end. The correction must happen before the first payroll run of the new fiscal year, not after.

TDS over-deducted during FY 2082-83 can be claimed as a refund when the annual tax return is filed for that year (due in Ashwin 2083). Employees whose employer deducted at 30% or 36% on upper income, but whose final computed tax is lower after deductions and credits are applied, are entitled to claim any overpayment. The new 2083-84 slabs do not retroactively reduce 2082-83 liability - they apply only from Shrawan 1, 2083 onward.

Payroll teams have three tasks to complete before Shrawan payroll runs. First, update the slab table in the payroll system to the new five brackets. Second, recalculate projected annual tax for each employee at their current salary package. Third, confirm whether any employees who previously fell below the Rs 5 lakh threshold now fall within the 1% band under the new Rs 10 lakh threshold - the number of employees requiring any TDS deduction at all may increase, even as the amounts drop. Businesses using payroll software should verify whether the vendor has pushed updated slab tables or whether manual entry is required - cross-check against the official IRD TMS portal publication before processing.

Payroll teams must update TDS slab tables before Shrawan payroll runs. An incorrect slab in month one carries through all 12 months and compounds the reconciliation work at year-end. Verify the update against the official IRD TMS portal publication - do not rely solely on vendor defaults or assumptions carried over from the previous year.

Tax Planning Under the New Structure - What Changes for Employees

The revised slabs change the value of several planning decisions that salaried employees typically make at the start of a fiscal year. The most immediately relevant is the allowable deduction for SSF voluntary contributions, life insurance premiums, and contributions to approved retirement funds. These deductions reduce taxable income before slabs are applied and have always been most valuable in high marginal brackets. With the top marginal rate now at 29% rather than the old surcharge peak of 39%, the after-tax saving from each rupee of qualifying deduction is lower at the extreme end - but still meaningful for earners above Rs 25 lakh.

Life insurance premiums up to Rs 40,000 per year remain a standard deductible item under the Income Tax Act 2058. SSF voluntary contributions beyond the mandatory rate are also deductible. Whether the 2083-84 Finance Act adjusts any of these limits or introduces new categories should be confirmed when the final Finance Act text is published. The budget speech summarises intent - the Finance Act, once passed, carries the binding provision.

For businesses that design salary packages, the wider 1% band simplifies structuring decisions. A total compensation package of Rs 10 lakh that was previously split across components to minimize the tax burden now sits entirely within one rate band. This matters most for small and mid-sized businesses in Kathmandu, Pokhara, and Birgunj that are formalizing payroll for the first time - the new structure is easier to explain to employees, easier to administer correctly, and produces far less TDS reconciliation variance at year-end when the actual numbers are closer to the projected ones.

The collapse of the 36% and 39% surcharge bands into a flat 29% means deductions are slightly less valuable at the extreme margin for high earners - but the total tax burden is substantially lower regardless. For businesses formalizing salary structures, wider bands mean fewer bracket transitions and fewer TDS computation errors across the year.

Earners above Rs 5 lakh immediately entered the 10% and then 20% band within a narrow range

The entire first Rs 10 lakh is taxed at 1% - a Rs 75,000 annual saving for any earner at that level

A mid-level manager earning Rs 12 lakh paid 30% on Rs 2 lakh - a steep jump for ordinary salaries

The 30% bracket is removed; what was the penultimate rate now starts Rs 15 lakh higher

Two surcharge bands stacked above Rs 20 lakh - senior salaries faced the highest effective rate with no ceiling

Both old surcharge rates are gone; one flat 29% applies to all income above Rs 40L with no further escalation

Five tight slabs meant small salary increments crossed rate thresholds, complicating TDS computation

Larger bands mean most salary ranges stay within one bracket for the full year - simpler TDS and fewer reconciliation errors

Effective rates of 36% and 39% on upper income made formally declaring senior compensation disproportionately expensive

A lower, single top rate reduces the gap between formal and informal compensation, supporting proper payroll compliance

Frequently Asked Questions

The new slabs apply from Shrawan 1, 2083 - the start of fiscal year 2083-84, which falls in mid-July 2026. Payslips and TDS calculations from that date onward must use the revised rates. Income earned in FY 2082-83 and the tax return filed in Ashwin 2083 for that year use the old structure, regardless of when payment is actually made or when the return is filed.

Not automatically in all cases. Some payroll software vendors push slab updates as part of a year-end release, but many Nepal businesses enter slab tables manually or use Excel-based payroll that requires direct edits. Employees should check their first Shrawan 2083 payslip - if the TDS deduction does not reflect the new slabs, raise it with finance or HR immediately. Under-deduction creates personal tax liability at year-end; over-deduction means waiting for a refund after filing. Either way, the employee bears the practical consequence if the slab table is not updated on time.

Standard allowable deductions under the Income Tax Act 2058 continue to apply alongside the new slabs. Common items for salaried individuals include life insurance premiums up to Rs 40,000 per year, SSF voluntary contributions beyond the mandatory rate, contributions to approved retirement funds, and donations to approved institutions. These deductions reduce your taxable income before the slab computation is applied. The Finance Act 2083-84 may adjust specific limits or introduce new categories - confirm the current list with IRD or a registered tax practitioner before computing your annual liability or submitting a return.

Take the Next Step

If your payroll system needs updating for the new tax slabs, or you want to review your team's TDS configuration before Shrawan 2083, speak with a tax professional or explore payroll tools built for Nepal compliance.